Why the Future of Fuel Retail Isn’t About Fuel

In traditional retail logic, a convenience store's competitive edge relies on network density, repeat purchases, and efficiency. Typical c-store networks pursue proactive site expansion, saturating commercial districts, residential areas, and office clusters. This density reinforces brand presence while spreading logistics and supply chain costs, ultimately creating scale advantages.

Gas station convenience stores, however, have always operated under a different logic. Their locations are not driven by retail opportunity but by infrastructure constraints: the store exists because the fuel station exists. Footfall is therefore not intentional retail traffic but scenario-triggered demand, activated by fueling or charging. In this sense, gas station retail represents one of the clearest examples of infrastructure-led retail.

Structural Shifts: Fuel Value Pools Are Contracting While Non-Fuel Expands

Against the backdrop of the global energy transition, the gas station business model is undergoing a massive structural transformation.

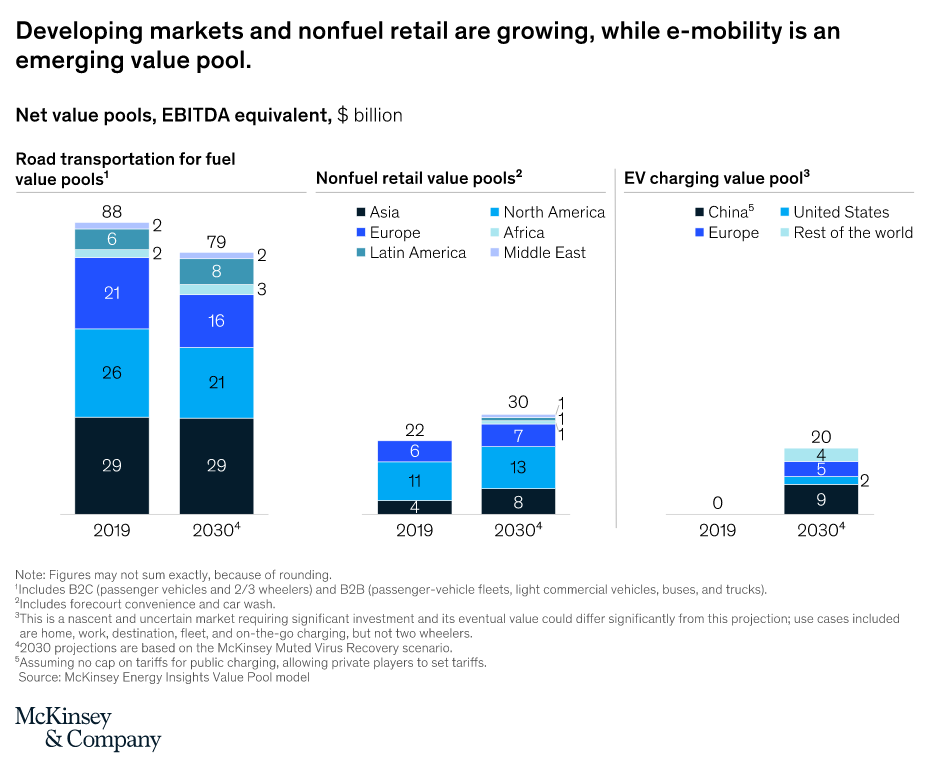

McKinsey & Company estimates that the global fossil fuel retail value pool will shrink from $88 billion in 2019 to $79 billion by 2030. Conversely, non-fuel retail is expanding across most markets. By 2030, non-fuel business in Asia is expected to grow by nearly 50% compared to 2019, making it the fastest-growing region.

Several forces are driving this shift:

Rapid EV adoption is structurally eroding fuel volumes

Persistent margin pressure is compressing energy retail spreads

Dwell time is expanding, moving the experience from “pump-and-go” to “stay-and-consume”

As a result, the industry’s logic is reversing. Historically, fuel traffic supported retail. Increasingly, retail economics support the station. Merchandising, foodservice, and service experience are becoming primary competitive differentiators for energy sites.

Mature Markets Have Already Moved Beyond Fuel

In mature markets, the transition toward non-fuel economics is well established.

Across Europe, Japan, and South Korea, more than 80% of stations include convenience retail, with non-fuel revenue accounting for roughly 40% of total sales.

The United States represents the most mature model. According to National Association of Convenience Stores, more than 90% of U.S. stations operate convenience stores. The integrated model of "gas station + fast food/coffee/auto repair" is the absolute mainstream, shifting the profit center from the outdoor pumps to the indoor shelves. The integrated model of "gas station + fast food/coffee/auto repair" is the absolute mainstream, shifting the profit center from the outdoor pumps to the indoor shelves.

By contrast, the Chinese market is characterized by massive scale but an immature profit structure.

In terms of physical footprint, Sinopec's Easy Joy operates approximately 28,000 stores, while PetroChina's uSmile operates over 20,000 locations.

Despite this massive volume, their profit structures lag behind overseas counterparts. Take Sinopec as an example: the company launched its non-fuel strategy in 2006, partnering with McDonald's for drive-thrus, founding Easy Joy in 2008, and entering the freshly brewed coffee market in 2019. According to its 2023 financial report, while non-fuel revenue reached tens of billions of RMB—accounting for just 2.3% of the marketing and distribution segment's total revenue—it generated roughly 18% of the segment's robust profit (exceeding RMB 4.5 billion).

This data reveals a massive momentum gap: the profit leverage of the non-fuel business is exceptionally high, making comprehensive operational efficiency upgrades an urgent priority.

The Path Forward: From Fueling Points to Lifestyle Infrastructure

The EV revolution is doing more than shifting energy sources; it is redefining the "dwell economy."

In traditional fueling scenarios, a driver typically takes 3 to 5 minutes to refuel. In EV charging scenarios, a 15-to-40-minute stay becomes the norm. This extended time window fundamentally raises the ceiling for product assortment, food offerings, and service combinations, reshaping the spatial value and commercial potential of the gas station.

Consequently, future gas stations must shed their label as singular energy facilities and evolve into super nodes that combine community transit hubs with driver lifestyle services.

Multi-Format Integration and the Rise of Scenario Assets

Gas stations are increasingly integrating foodservice, automotive services, community services, parcel handling, and micro-fulfillment capabilities. Operating models are shifting toward shop-in-shop, leasing, partnerships, and platform ecosystems.

This marks a structural shift: energy infrastructure is being reinterpreted as scenario infrastructure — assets designed to capture time, not just transactions.

Becoming the Infrastructure for Instant Retail

Integration with on-demand retail is emerging as a major source of forecourt value. With dense networks, strategic roadside locations, convenient parking, and built-in fulfillment readiness, gas stations are uniquely positioned to operate as last-mile nodes.

The partnership between a leading Chinese delivery platform and Easy Joy illustrates this shift, reframing station networks as distributed infrastructure for instant retail. In this model, the forecourt moves beyond fueling, becoming embedded in the city’s logistics layer as both a consumer touchpoint and a fulfillment asset.

Digital Intelligence as the Capability Ceiling

In this evolution, digital intelligence is no longer just an efficiency tool; it is the core capability that dictates a retailer's upper limit.

To navigate this shift, Sinopec’s Easy Joy partnered with Dmall to comprehensively digitize its store operations. By implementing DMALL's end-to-end retail operating system, Easy Joy has unlocked data-driven execution spanning assortment, merchandising, and checkout. By dynamically optimizing product structures based on historical sales and precise driver profiles, and reducing checkout friction via smart self-service terminals, this digital infrastructure directly elevates conversion rates and maximizes single-store efficiency.

Dynamic Intervention in the User Journey

The deeper transformation lies in user operations. The endgame of gas station digitalization is the construction of an integrated platform spanning "people, vehicles, and life." By unifying data across fueling, charging, dining, and retail, a "register once, use everywhere" service ecosystem is realized. Under this framework, retail no longer relies on random purchases but uses dynamic interventions based on the consumer journey.

When a driver initiates charging, the system identifies the estimated dwell time and matches tailored consumption plans accordingly. This transforms passive waiting time into a highly operational, high-margin consumption window.

Conclusion

The evolution of gas station retail reflects a broader convergence between physical infrastructure and local lifestyle services.

Future forecourts will simultaneously function as energy networks, fulfillment networks, and retail networks. Their value will be defined less by fuel throughput and more by how effectively operators manage dwell time, scenarios, and customer relationships.

The gas station convenience store is no longer a peripheral add-on. It is emerging as one of the most strategically important formats in infrastructure-led retail and one of the most promising offline super nodes of the digital era.